Understanding the Reverse Repurchase Agreement and Its Role in Preventing Bank Runs

Introduction

In March 2023, the Federal Reserve implemented a reverse-repo facility to address the losses on the balance sheet, resulting from low interest rates and increased investments in longer-dated bonds, as bond prices rose, the value of the long-dated bonds, held by US banks, fell. This article aims to explain the concept of reverse repurchase agreements and discuss how they were used to prevent further runs on the banking system.

I also want to examine the Feds various policies and strategies influenced by economic theories and lessons learned from historical examples. Additionally, the article examines the Federal Reserve's policy stance and the implications of maintaining large deficits without proportional economic growth. Historical instances of failed Treasury auctions shedding light on the importance of monetary and fiscal responses. The aim is to gain a comprehensive understanding of these complex economic concepts and their potential impacts on consumers, fiscal stability, and the integrity of the financial system. While at the same time, trying to create progressive solutions to the current impasse.

What is a Reverse Repo?

A reverse repurchase agreement, commonly known as a reverse repo, is a financial transaction in which the Federal Reserve purchases securities from financial institutions, such as banks and money market funds, with an agreement to sell them back at a later date. In return, these institutions deposit reserves at the Fed, earning interest in the form of the reverse repo rate.

Low Interest Rates and Increased Capital Availability

Since the financial crisis of 2008, interest rates have remained at historically low levels. This has increased the availability of capital for banks, making it cheaper for them to borrow money and invest in the real economy.

Quantitative easing (QE) refers to a monetary policy tool used by central banks to stimulate economic growth and increase liquidity in the financial system. During QE, central banks purchase government bonds or other financial assets from banks and financial institutions. This injection of money into the economy aims to lower interest rates and encourage lending and investment.

When central banks purchase assets from banks through QE, the banks receive cash in exchange for the assets. This increases the cash reserves on the banks' balance sheet and provides additional liquidity, due to the duration of QE, banks took greater risks with the liquidity provided by QE.

Banks typically hold bonds and other fixed-income securities as part of their investment portfolio. These assets generate interest income for the banks. When interest rates are low, as they have been since the financial crisis, the yields on these bonds also diminish. This reduction in interest income can impact the banks' profitability and overall financial performance.

Banks also have to hold a certain amount of Tier 1 capital on their balance sheet. This refers to the highest quality capital that banks need to maintain to withstand financial stresses. Tier 1 capital consists of core capital elements, such as AAA rated bonds and retained earnings, on their balance sheet, which can absorb losses without the bank becoming insolvent. Regulatory authorities impose certain minimum capital requirements to ensure banks' stability and ability to absorb losses.

To maximise returns, some banks increased the longevity of their investments, including bonds, which means holding them for longer durations. By extending the maturity of their bonds, banks aim to lock in higher yields for a longer period. However, this strategy can also expose the banks to interest rate risk.

When interest rates rise, the market value of existing bonds with lower yields decreases. This results in a potential loss for banks that hold these bonds. The loss arises from the difference between the market value and the original purchase price. The can negatively impact the banks' balance sheet and profitability, especially if customers start liquidating their balance sheet with their bank, as happened in March with Signature and Silicon Valley Bank.

What risk management tools should these banks use?

Banks should have employed risk management strategies, such as diversification and hedging, to mitigate potential losses as the Federal Reserve started to pivot and raise interest rates.

Diversification, spreading their investments across different asset classes would of reduce concentration risk. By diversifying their portfolio, banks can decrease the impact of any single investment's loss on their overall financial position. For example, instead of solely holding bonds, banks could have diversified into things like Gold and real estate, which may have given the banks retained earnings, in the form of rent or Gold, which could have performed better under rising interest rates.

Additionally, hedging strategies could have been employed by the banks to protect against potential losses. Hedging involves taking offsetting positions that mitigate the impact of adverse price movements. In the case of rising interest rates, banks could have used interest rate swaps or options to hedge against the negative impact on their bond holdings. By taking short positions or purchasing options contracts, banks could have reduced the risk of losing value in their bond portfolios as rates increased.

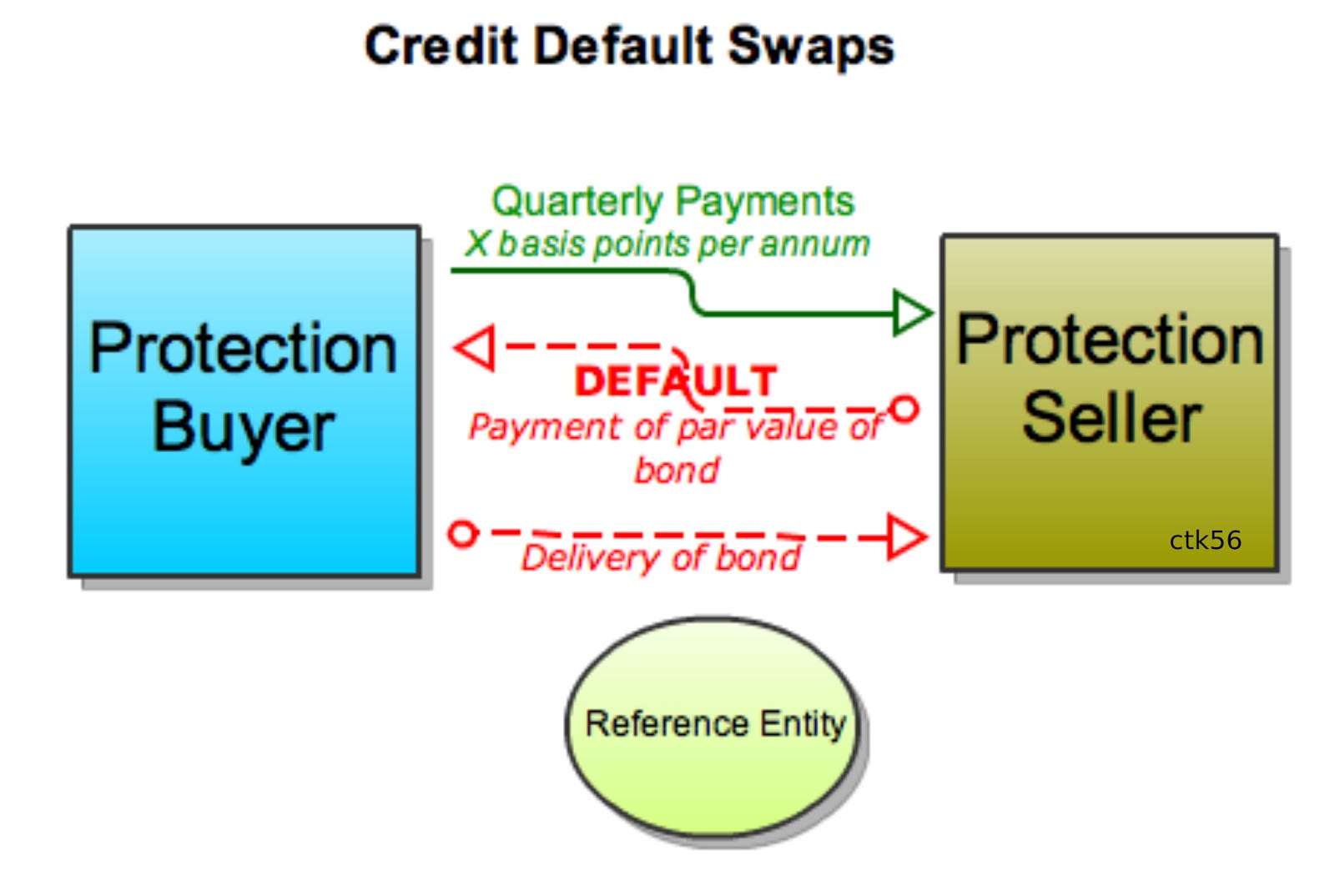

Another risk management approach that banks could have considered is taking out insurance or utilising credit default swaps (CDS). These financial instruments can provide protection against potential losses in bond values. By purchasing insurance or entering into CDS contracts, banks could have transferred the risk of rising interest rates and potential bond market losses to other parties, minimising the impact on their balance sheets.

While hindsight is also a great thing, it is clear some banks did not adequately implement effective risk management strategies or adequately anticipated the impact of rising interest rates on the market value of their bond holdings. As a result, the loss on the banks' balance sheets due to the market value of bonds increased, highlighting the importance of proactive risk management in such situations.

The Collapse of Banks and the Reverse Repo Solution

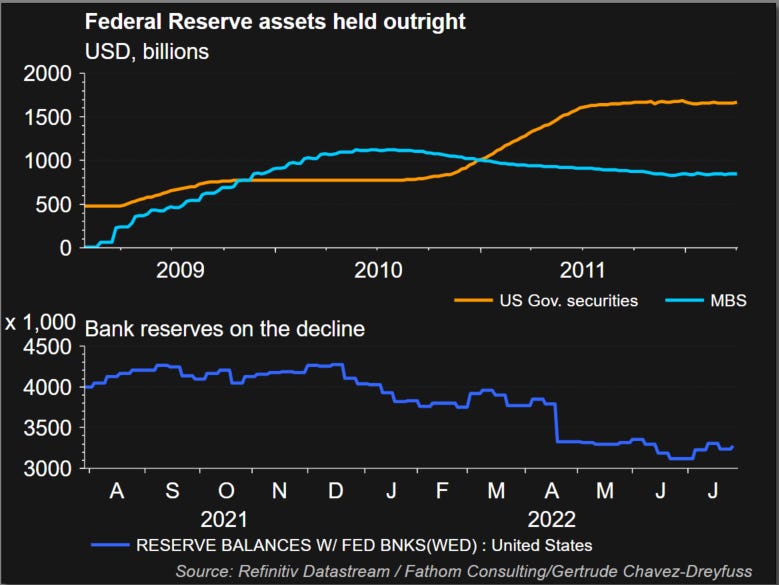

As the Federal Reserve rapidly increased interest rates from under 1% to its current level of 5.25-5.5%, banks holding substantial portfolios of longer-dated bonds experienced significant losses. This, coupled with customer concerns about a possible bank run, led to a collapse of banks like SVB. As a result, the Federal Reserve used the Reverse-Repo system to remove long-term bonds from the bank's balance sheet for a short period of time, at the nominal rank of the bond.

This was a short term measure to prevent further runs on the banking system and stabilise the interbank market. In this process, shadow banks, including money-market funds, the reverse repurchase agreement conducted by the banks, also called “RRP,” is a transaction in which the banks sells its long-term bond to an eligible counterparty (Fed) with an agreement to repurchase that same bond at a specified price at a specific time in the future. This reversed the flow of capital, draining excess deposits from the financial system.

By establishing a floor on the banks balance sheet and the interbank market, the reverse repo system helped the Federal Reserve in its efforts to exit from ultra-low interest rates, while stabilising the banking system. As it reduced the risk of bank runs by providing a reliable funding source through reverse repurchase agreements. It aso allowed banks to address their losses on longer-dated bonds in a controlled manner, avoiding sudden and drastic liquidations that could further destabilise the financial system.

Challenges Faced by the Federal Reserve

While the reverse repo system implemented by the Federal Reserve stabilised the banking system and prevent further bank runs, it did have some unintended consequences. One of the main issues was the added money supply to the system during a time when the Fed was trying to tighten the money supply. This was due to the fact that when banks engaged in reverse repurchase agreements with the Fed, they effectively received cash in exchange for their long-term bonds. This increased the overall money supply in the system.

Additionally, the fiscal spending by the US Treasury, carrying a deficit of 8% of GDP, also contributed to the increase in the money supply. This combination of monetary and fiscal policy actions led to an increase in the overall money supply, which in turn had an impact on inflation.

As a result, the Consumer Price Index (CPI), which measures the average change in prices over time for a basket of goods and services, skyrocketed to a high of 9.9%. This was a significant increase in inflation and caused concerns among consumers and economic analysts alike.

It is important to note that these issues were the result of a combination of factors, including the rapid increase in interest rates, bank collapses, and the subsequent reverse repo system. The impact of these actions on inflation was not solely due to the reverse repo system alone but was also influenced by other economic factors, such as fiscal policy decisions.

However, this does lead us to ask, what policies are needed to address these issues and ensure the stability of the financial system while managing inflationary pressures?

The Federal Reserve Policy Response

The Federal Reserve has a dual mandate of maintaining price stability and achieving maximum employment. However, several challenges have emerged in meeting these objectives. Consumer Price Index (CPI) is currently above the target rate of 2%, at 3.2%, while jobless claims are below 4%. The Fed's dovish pivot, despite these challenges, raises questions about the prioritisation of its policy objectives.

The Federal Reserve's decision-making process may be influenced by the Treasury Department's impending debt issuances and auctions. The dovish pivot and the need for overnight funding outside traditional market mechanisms suggest that the current value of the Fed's mandate is in question. As a result, in the coming year, the Fed may need to inject additional liquidity into the reverse-repo system or consider reducing interest rates to prevent a drying up of liquidity in the economy.

The escalating budget deficit raises concerns about the lack of fiscal responsibility. The Treasury's efforts to address the $1.7 trillion deficit through increased debt issuance add to this concern. While the Fed may support Treasury auctions through accommodative monetary policy, it is crucial for policymakers to address the root causes of the deficit. The absence of concerted efforts to ensure fiscal responsibility raises questions about the long-term sustainability of government finances and the Fed's ability to support such fiscal expansion.

Policy Opinions of the Federal Reserve

Maintaining large deficits without proportional economic growth or an expansion of natural resource production can strain fiscal stability and lead to inflationary pressures. As the government continues to finance its obligations through increased borrowing, consumers may face higher interest rates on loans, impacting personal finances and economic growth.

In the current economic environment, both the Federal Reserve and the US government should pursue prudent policy decisions to address the imbalance between the supply of money and the value of production. This can be achieved through supply-side policy reforms that complement the Federal Reserve's efforts to cool down demand through monetary tightening.

Firstly, reducing government spending would help dampen demand-fueled inflation. By reducing the demand for goods and services, this would create a balance between the supply of money and the supply of resources in the economy. Additionally, it would restore confidence in the government's ability to manage its debt and control inflation expectations.

Secondly, removing barriers to work through occupational licensing reform, increased work flexibility, and reducing work disincentives in tax and transfer programs would incentivize more people to participate in the labour force. This would increase the supply of labour, reducing the cost of production for businesses and contributing to a more balanced economy.

Thirdly, deregulation in energy, housing, and other markets would lower the regulatory burden on businesses. This would decrease the cost of domestic production and result in lower prices for consumers, fostering a more balanced and competitive market environment.

Lastly, reducing tariffs and eliminating regulatory barriers, such as the Jones Act and Foreign Dredge Act, would facilitate international trade. This would provide consumers with access to cheaper goods and increase the resiliency of supply chains, ensuring a diverse range of options at competitive prices.

By implementing these supply-side policy reforms, the US government and the Federal Reserve can enable market forces to create equilibrium between the supply of money and the value of production in the economy. This approach does not rely on fiscal or monetary expansion but rather focuses on creating the necessary conditions for market-driven equilibrium. But I must stress without a strategic and diverse approach, the Treasury really does risk the chance of facing failed Treasury auctions.

Lessons from Failed Treasury Auctions

To emphasise this point we need to understand the historical examples of failed Treasury auctions to demonstrate the potential risks when government debt raises concerns among investors. The United States experienced failed Treasury auctions in 2009 and 2011, which posed challenges for raising funds through the sale of Treasury securities. These instances necessitated both monetary and fiscal responses to address the issues.

The monetary response to failed Treasury auctions included the implementation of Quantitative Easing (QE) by the Federal Reserve. QE involved expanding the money supply to stimulate the economy. On the fiscal front, the response involved expanding economic growth through increased government spending.

The expansion of the money supply through QE and the level of debt resulting from fiscal expansion have made the Federal Reserve apprehensive about potential future failed auctions. Concerns about the integrity of the financial system and the dollar as a global reserve currency likely influence the Fed's decisions and may explain recent shifts in monetary policy. While the FederalReserveis running a tightrope, the Federal Reserve must not get caught in a debt trap, like the one the BOJ is currently in.

Lessons from the Bank of Japan (BOJ)

The Federal Reserve's approach, resembling that of the BOJ, which has implemented policies such as near-zero yields, carries certain dangers. The BOJ's course of action has led to a debt spiral, raising concerns about the long-term sustainability of government finances. Despite the costs associated with such measures, the Fed's priority appears to be avoiding another failed auction.

It is vital to consider the potential dangers associated with excessive debt accumulation, as evident from the debt spiral that the BOJ currently faces. To mitigate these risks and ensure sustainable economic growth, the Federal Reserve must adopt a prudent policy response characterised by a delicate balance between providing liquidity and addressing fiscal responsibility. This approach has also led to the depreciation of the Japanese yen, increased import costs, and inflationary pressures.

To avoid similar pitfalls, the Federal Reserve must carefully analyse the consequences of the BOJ's policies and adopt a more creative and nuanced approach. Simply replicating the BOJ's strategy of zero interest rates at all costs is clearly not effective in the long-term in addressing the current fiscal and monetary challenges.

The Federal Reserve should prioritise finding a delicate balance between providing liquidity and ensuring fiscal responsibility. This requires a comprehensive assessment of the potential risks and benefits associated with different policy options. Seeking collaboration and support from the Treasury can also help in developing a more robust and sustainable approach that aligns with the broader objectives of price stability, maximum employment, and long-term fiscal sustainability.

By learning from the BOJ's experiences and taking a more careful and analytical approach, the Federal Reserve can avoid falling into a debt spiral and mitigate the risks associated with excessive debt accumulation. This will contribute to maintaining the integrity of the financial system, promoting sustainable economic growth, and safeguarding the long-term stability of government finances.

Conclusion

In conclusion, addressing the fiscal and monetary issues faced by the Federal Reserve and the Treasury requires a multifaceted solution. It is crucial to strike a balance between maintaining the credibility of the dollar as a global reserve currency and supporting sustainable economic development.

Firstly, implementing measures to avoid excessive debt accumulation is vital. This can be achieved through prudent fiscal management and reducing government spending. Tamping down on demand-fueled inflation and restoring confidence in the government's ability to pay down debt will play a significant role in controlling inflation expectations.

Secondly, fostering proportional economic growth is necessary. Removing barriers to work, such as occupational licensing reform and tax and transfer program adjustments, can increase labor force participation and reduce production costs for businesses. Deregulation of various markets, including energy and housing, can also lower domestic production costs and improve supply chain resilience.

Lastly, ensuring that monetary and fiscal policies align with broader objectives of price stability, maximum employment, and long-term fiscal sustainability is essential. The Federal Reserve should carefully consider the impacts of its monetary policy decisions on inflation, interest rates, and liquidity provision. Close coordination between monetary policymakers and fiscal authorities will be crucial in maintaining financial stability, promoting sustainable growth, and safeguarding the integrity of the global economy.

By implementing these measures in a comprehensive and balanced manner, the Federal Reserve and the Treasury can address the current fiscal and monetary issues, mitigate risks to the financial system, and support long-term economic stability and growth.