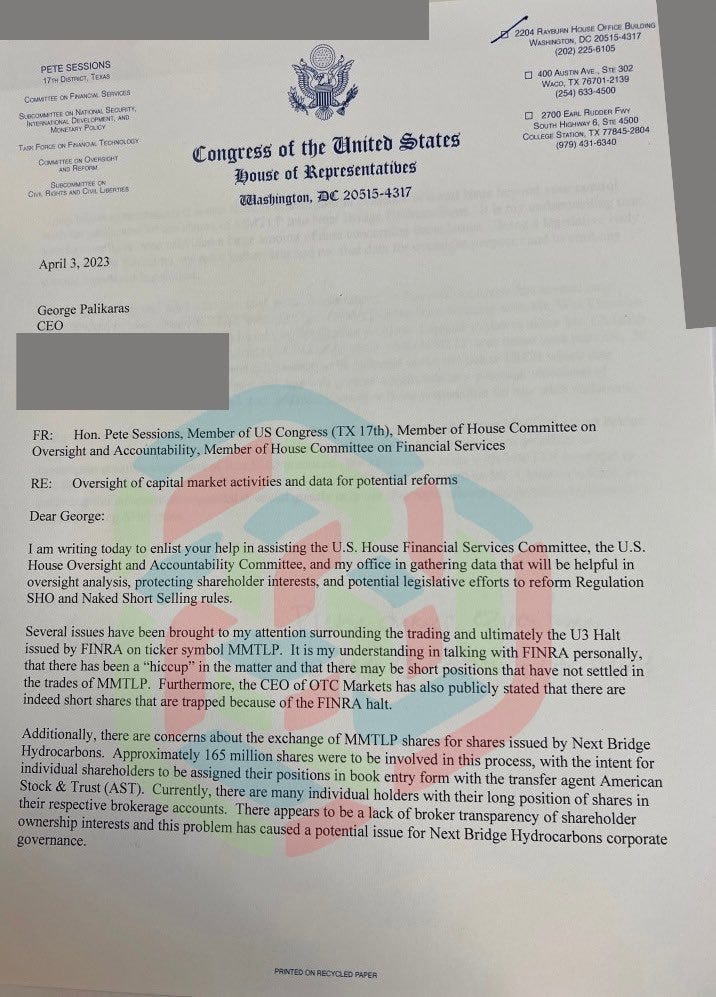

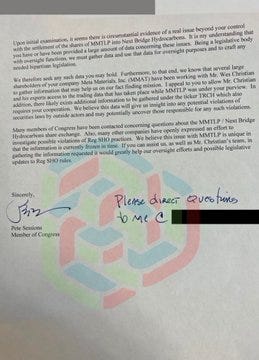

The MMTLP Fraud is at its heart a failure to secure the integrity of the securities ledger and has raised serious concerns amongst Investors, but most importantly the MMTLP community. This has prompted Congress to take a closer look at the issue, and specifically, at the importance of the Bluesheets.

Bluesheets are records of all trades and transactions related to shares, and having access to them can bring clarity and transparency to the issue at hand. Nowhere is this more critical than in the case of MMTLP shares, where a lack of clarity around their cancellation has left investors scratching their heads. In this context, understanding the importance of Bluesheets is key to understanding how the issue can be resolved.

The MMTLP Corporate Action

The corporate action taken by Meta Materials, which involved distribution of the common stock of its wholly owned subsidiary, Next Bridge Hydrocarbons, Inc. The Series A Preferred Shares of Meta Materials, which were originally unlisted, became listed on the OTC market under the symbol MMTLP.

Meta Materials later announced that it would be distributing one share of Next Bridge common stock to each shareholder of its Series A Preferred Shares (MMTLP). This distribution was scheduled for December 14, 2022, at which time the MMTLP shares would be cancelled, and shareholders would no longer have any rights with respect to them. Any purchases made after December 8, 2022, would not be eligible to receive Next Bridge shares in the distribution. FINRA halted trading in MMTLP on December 9, 2022.

Bluesheets are industry records that contain information about transactions executed by broker-dealers at the National Association of Securities Dealers (NASD). These records are used by regulatory bodies, such as the Securities and Exchange Commission (SEC), to investigate potential insider trading, market manipulation, and other illegal activities in the securities market.

1. Why did FINRA halt trading in MMTLP?

FINRA halted trading in MMTLP because it determined that the corporate action taken by Meta Materials, specifically the distribution of Next Bridge common stock and cancellation of MMTLP shares, could potentially cause major disruption to the marketplace and significant uncertainty in the settlement and clearance process. After December 12, MMTLP shares would no longer be DTC-eligible, and Next Bridge common stock was not expected to be DTC-eligible, which raised concerns about how transactions executed after December 8 would settle in an orderly manner. Trading in MMTLP was halted to protect investors from potentially buying shares that would soon be cancelled, and to ensure that holders of MMTLP shares could receive Next Bridge common stock in the distribution if they were eligible to do so.

2. Why did FINRA halt trading on December 9 if shareholders as of December 12 were entitled to receive the Next Bridge distribution?

FINRA halted trading in MMTLP on December 9 because securities transactions typically must settle within two business days. This meant that trades executed on or before December 8 would settle in time to establish the purchaser as a new holder of the shares as of December 12, which was the date used to determine eligibility for the Next Bridge distribution. Trades executed after December 8 were not guaranteed to settle before the MMTLP shares were cancelled on December 14, which created uncertainty about the ability of buyers to receive Next Bridge shares and settle their trades in an orderly manner. Therefore, FINRA halted trading in MMTLP to protect investors who may have unknowingly purchased shares that would be cancelled and to ensure an orderly settlement process.

3. Has the MMTLP trading halt ended?

Yes, the MMTLP trading halt ended on December 13, 2022, concurrent with FINRA's deletion of the MMTLP symbol. This was confirmed in a notice published on December 9, 2022. FINRA's website was updated on February 16, 2023, to reflect the end of the trading halt. However, the MMTLP shares were cancelled by the issuer on December 14, 2022, and have not been tradeable since that time regardless of the halt status displayed on FINRA's website.

Therefore, shareholders of MMTLP securities are no longer able to trade these shares and their only recourse is to receive Next Bridge common stock, if they were eligible for the distribution, according to the terms of the corporate action taken by Meta Materials.

4. How were MMTLP shares publicly quoted and traded in the first place?

MMTLP shares became publicly quoted and traded because Meta Materials issued the Series A Preferred Shares in connection with their merger with Torchlight Energy Resources, and the shares were then sold to investors who wanted to trade them on the OTC market. Although FINRA does not approve or determine when broker-dealers or customers may begin trading securities, they do require firms to report executed transactions. When there is no symbol for a security, broker-dealers may request one from FINRA to facilitate electronic reporting. In this case, a broker-dealer requested a symbol for MMTLP to facilitate trade reporting of executed transactions. However, it's important to note that the process for trade reporting is separate from the process for quoting a security on a broker-dealer's own behalf, which requires a review of specified information about the issuing company under SEC Rule 15c2-11. In this case, broker-dealers relied on an exception to SEC Rule 15c2-11 that permits the publication of a quotation for unsolicited customer orders.

5. Did FINRA cancel the MMTLP shares? Did FINRA delete the MMTLP symbol?

FINRA did not cancel the MMTLP shares, as that was an action taken by the issuer, Meta Materials. Additionally, FINRA is not able to cancel any securities that are issued by a company. However, FINRA assigned and later deleted the MMTLP symbol, as is the case with any symbol assigned to an unlisted security, in this case on December 13, in accordance with the announcement made by Meta Materials about the imminent cancellation of the MMTLP shares effective December 14 in connection with the Next Bridge / MMTLP corporate action. Although FINRA deleted the MMTLP symbol, this does not affect the fact that the MMTLP shares were subsequently cancelled by Meta Materials, and can no longer be traded or reinstated.

6. What happened to investors who did not sell their MMTLP shares prior to the trading halt?

FINRA did not cancel the MMTLP shares, as that was an action taken by the issuer, Meta Materials. Additionally, FINRA is not able to cancel any securities that are issued by a company. However, FINRA assigned and later deleted the MMTLP symbol, as is the case with any symbol assigned to an unlisted security, in this case on December 13, in accordance with the announcement made by Meta Materials about the imminent cancellation of the MMTLP shares effective December 14 in connection with the Next Bridge / MMTLP corporate action. Although FINRA deleted the MMTLP symbol, this does not affect the fact that the MMTLP shares were subsequently cancelled by Meta Materials, and can no longer be traded or reinstated.

7. What would have happened to any trades executed after December 8 had FINRA not halted trading in MMTLP?

If FINRA had not halted trading in MMTLP, any trades executed after December 8 would not have settled in time for the buyer to become a holder of the MMTLP shares by December 12. These trades would have needed to be resolved through broker-to-broker processes outside of DTC, creating potential confusion and disagreement among the parties. Furthermore, there was concern that the MMTLP shares may have been cancelled by the issuer before broker-to-broker settlement occurred.

8. Is there public data concerning short sale activity in MMTLP?

The total short sale volume for transactions in MMTLP that settled from November 16, 2022, through November 30, 2022, was 7,413,679 shares, the published short interest for MMTLP on settlement date November 30, 2022, was 4,658,068 shares.

There are public data sets published by FINRA and the SEC that include short sale activity for MMTLP. FINRA publishes short interest reports that reflect short positions held on a given settlement date and are available on the FINRA website. FINRA also publishes daily short sale volume data by security for OTC equity securities. It's important to note that short sale volume activity and short interest reports are not the same, with differences expected for a variety of reasons, including the covering of short sales or short sale transactions executed solely to facilitate customer long sales. Therefore, investors are encouraged to review information on the differences between these two data sets.

9. Fails-to-Deliver

The SEC publishes data on "fails-to-deliver," which can occur as a result of either a long or a short sale. Fails-to-deliver can result from a "naked" short sale or a long sale where there was a delay in share delivery within the standard settlement period. SEC Regulation SHO imposes close-out requirements for fails-to-deliver in equity securities, including close-outs of fails-to-deliver in threshold securities. FINRA has a separate rule for the securities of issuers that are not SEC-reporting companies.

Due to a systems coding issue, FINRA incorrectly classified MMTLP as the security of a non-SEC-reporting company and published its "Threshold Securities List" incorrectly, from October 22, 2021, through January 4, 2022, and from October 17, 2022, through December 13, 2022. MMTLP did not have fails-to-deliver that would have rendered it a threshold security under Regulation SHO, and it was an error to publish it on the list. FINRA has removed MMTLP from the Threshold Securities List.

10. What happens if short positions in MMTLP were not closed out before FINRA halted trading?

Broker-dealers have operational conventions in place for adjusting short positions following a corporate action. In this instance, FINRA understands that firms have adjusted short positions in MMTLP to reflect an equal size short position in Next Bridge (i.e., an account with a short position of 100 shares of MMTLP now reflects a short position of 100 shares of Next Bridge). In other words, the corporate action did not compel short positions to be closed or extinguish any obligations associated with outstanding short positions.

The issue is a failure of FINRA to secure the integrity of the securities ledger and that having access to the bluesheet can bring clarity and transparency to the issue and is the reason why Congress is so interested in the Bluesheets.

Having access to the bluesheet can bring clarity and transparency to the issue because it provides a record of all trades and transactions related to the MMTLP shares. With this information, regulators and investors can better understand what happened to these shares and why they were cancelled.

What are bluesheets?

Bluesheets are comprehensive reports that licensed securities broker-dealers are required to provide upon request to regulatory bodies such as the Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA). These reports contain detailed information about a firm's trading activity, including the identity of the customer, the security traded, the date and time of the transaction, the price at which the security was traded, and any other relevant information.

The purpose of bluesheets is to help regulators and enforcement agencies monitor and investigate potential securities violations such as insider trading, market manipulation, and other fraudulent activities. By analyzing this data, regulators can identify patterns of suspicious activity and take action to protect investors and maintain the integrity of the financial markets.

How to gain access to bluesheets?

To gain access and control over bluesheets, broker-dealers are required to comply with regulations and reporting requirements put in place by regulatory bodies such as the SEC. Broker-dealers must maintain accurate and timely records of their trading activities, which include details about the securities traded, the parties involved in the transaction, and the time and date of the trade. These records must be made readily accessible to regulators and other authorized parties upon request.

Regulators have the authority to request and review bluesheets as part of their investigations into potential securities fraud or illegal activity. The SEC, for example, has the power to subpoena broker-dealers for their bluesheets and other trading records. In cases where broker-dealers fail to provide access to their bluesheets or maintain inaccurate or incomplete records, they may face regulatory penalties and fines.

Can a company request their bluesheets?

A company can request its own bluesheets. Broker-dealers are required to maintain accurate and up-to-date records of their trading activities, including details of the securities traded, parties involved in the transaction, and the time and date of the trade. This information is also provided to regulatory bodies upon request to help monitor the market and ensure compliance with regulations.

When a company request its own bluesheets, they typically do so to review their own trading activities for compliance purposes, audit, or internal control purposes. The company will need to request these records from their broker-dealer, who is responsible for maintaining and providing access to these records upon request.

It's important to note that while companies can request their own bluesheets, they are not entitled to request the bluesheets of other broker-dealers or other companies. Other entities can only request access to these records under certain circumstances, such as a regulatory investigation for potential securities fraud or market manipulation.

Who has control over the securities ledger?

In the securities industry, control over the ledger used for clearing and settlement of securities is typically divided between various entities involved in the process. The specific entities involved may vary depending on the market and jurisdiction, but typically include:

1. Stock Exchanges - Stock exchanges provide a platform for the trading of securities, and is typically where the orders to buy and sell securities are executed.

2. Clearinghouses - Clearinghouses are intermediaries between buyers and sellers of securities, ensuring that trades settle in a timely and orderly way. Clearinghouses act as central counterparties, standing between buyers and sellers, and managing the risk associated with buying and selling securities.

3. Custodians - Custodian banks receive and hold assets on behalf of their clients, providing secure storage of securities and ensuring that they are properly transferred between investors.

4. Settlement Agents - Settlement agents are responsible for the final process of exchanging funds for securities between the parties involved in a transaction.

The ledger that is used for clearing and settlement of securities is typically maintained by the various entities involved, and each of these entities has different levels of control and responsibility over the process. However, most markets have strict regulatory requirements and standard processes in place to ensure that the ledger is accurate and reliable, reducing the risk of errors or fraud in the clearing and settlement process.

Control and integrity of the ledger

The ledger used for this process is typically divided among these entities, including stock exchanges, clearinghouses, custodians, and settlement agents.Each of these entities has a specific role in the process, such as providing platforms for trading securities or managing the risk associated with buying and selling securities.

However, the reality is as described by the $MMTLP fruad, this process is inefficient, lacks transparency and account ability and is continually infected by fruad.

Conflict of interest between broker and client

The Goldman Sachs fraud in the 2008 Global Financial Crisis (GFC) involved the sale of mortgage-backed securities (MBS) that were marketed to investors while the bank simultaneously bet against the same securities. This highlights the potential for a conflict of interest between the broker (Goldman Sachs) and client (investors).

In this case, Goldman Sachs had a duty to act in the best interests of its clients by recommending the MBS as a sound investment opportunity while it also had a financial incentive to bet against the same securities. This conflict of interest led to the bank making significant profits while investors suffered losses.

The Goldman Sachs case demonstrates the importance of disclosure and transparency in the financial industry, but also highlight in inabilityof the financialindustryto self-regulat. It also highlights the need for regulatory oversight to prevent such conflicts of interest and protect investors' interests. We must understand the human nature of the financial service industry, which itself serves as a cautionary tale of the consequences of disregarding ethical behavior and putting profits above clients' interests.

Is Artificial Intelligence (AI) and blockchain technology the solution

Artificial Intelligence (AI) and blockchain technology have the potential to make the clearing and settlement of securities more efficient by improving accuracy, speed, and transparency in the process. Here are some ways AI and blockchain technology could improve the process:

1. Improved accuracy: AI can be utilized to automatically verify data, detect anomalies, and respond to exceptions in real-time. This can lead to more accurate and efficient record-keeping throughout the clearing and settlement process.

2. Faster processing: Blockchain technology can ensure near-instantaneous processing of transactions, reducing the time required for trade settlement. Smart contracts that utilize blockchain technology can automate some of the processes currently handled manually by intermediaries, reducing the need for human intervention and increasing the efficiency of the process.

3. Greater transparency: The use of blockchain technology can provide a secure and tamper-proof record of all transactions, providing increased transparency and reducing the risk of fraudulent activities. Additionally, AI can be used to analyze the data contained in these records to uncover meaningful insights into the market and enhance regulatory oversight.

4. Reduced costs: The use of AI and blockchain technology can automate routine processes, reduce errors, and eliminate intermediaries, leading to lower costs in the settlement process.

The combination of AI and blockchain technology could lead to a more efficient, transparent, and cost-effective clearing and settlement process for securities, making the system so efficient that there is no reason for brokers self-regulate. However, there are still technological and regulatory challenges that need to be addressed before widespread adoption can occur.

DTCC (Depository Trust & Clearing Corporation) Project ION

DTCC launched ION in August 2022 as an industry-wide initiative to develop a next-generation post-trade platform. ION aims to leverage distributed ledger technology (DLT) to create a single industry-wide ecosystem for post-trade processing, including trade matching, clearing, and settlement.

The aim of ION is to create a more efficient and streamlined post-trade processing system that can reduce costs, improve transparency, and enhance risk management capabilities. It includes a broad range of participants from across the industry, including banks, broker-dealers, asset managers, market infrastructures, and service providers.

Could Project ION be the answer to naked short selling?

ION is not designed to address the specific issue of naked short selling. However, the project's implementation has the potential to contribute to broader efforts to increase transparency and oversight in the securities industry. By improving the post-trade processing of securities, ION could enable regulators to more effectively detect and prevent market manipulation, including naked short selling. Ultimately, the effectiveness of the solution will depend on the specific regulatory frameworks in place and the industry's willingness to adopt the new platform.

Naked short selling is a practice that is regulatory problem that requires the oversight of regulatory bodies as it involves an illegal activity that violates rules and regulations in the securities industry. Therefore, it is not necessarily the responsibility of DTCC's ION project to prevent this practice.

However, the implementation of ION can contribute to broader efforts to reduce the risk of fraudulent activities and increase transparency in the securities industry. One significant benefit of the ION project is that it enables the creation of a single industry-wide ecosystem for post-trade processing that can provide real-time data for transparency and efficient tracking of securities throughout the trading process.

In terms of specific risk management processes related to naked short selling, one approach could be to integrate sophisticated reporting systems to detect any potential naked short selling activities. This system could monitor market activity and reporting collateral levels to regulators continuously. Additionally, smart contracts may also be utilized to provide a structure for conveying, confirming, validating, and enforcing obligations throughout the securities trade lifecycle.

Ultimately, risk management processes designed to prevent naked short selling will depend on the specific regulatory frameworks in place and the industry's willingness to adopt new technologies and platforms like the recently launched DTCC's ION project.

Conclusion

The cases of Goldman Sachs during the Global Financial Crisis (GFC) and the short selling of $MMTLP illustrate the potential conflicts of interest that can arise between brokers and clients, leading to concerns about trusting brokers to clear and settle their customers' securities.

In the case of Goldman Sachs, the bank marketed mortgage-backed securities (MBS) to clients while simultaneously betting against them, causing losses for investors. This highlights the conflict of interest between the bank's duty to act in the best interests of its clients and its own financial incentives.

Similarly, in the $MMTLP short selling case, brokers were simultaneously representing both the borrower and the lender, leading to a scenario where the brokerage firm profited from the failure of the borrower to deliver the securities. This resulted in a claim by the lender against the brokerage firm for breach of fiduciary duty.

These cases demonstrate the need for greater regulation and oversight of brokers and underline the importance of transparency and ethical behavior in the financial industry. They suggest that the conflict of interest between brokers and clients makes it difficult to trust them to consistently act in the best interests of their clients when it comes to clearing and settling securities.

With specific regulatory frameworks in place and the industry's willingness to adopt new technologies and platforms like the recently launched DTCC's ION project could provide an effect solution.

Daniel’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.